So we take our last 8,000 of depreciation expense and check this part out, 32,000 plus 8,000, our accumulated depreciation is 40,000. Our depreciable base was the numerator in our equation, the cost minus residual value. So our cost of 42,000 minus our residual value of 2,000 is 40,000, right? And that after the 5 years, we’ve taken all of that depreciable base over the 5-year life. So here our total accumulated depreciation that we’ve taken over the life is 40,000. So it all works out here and guess what’s left in our net book value?

المحتوي

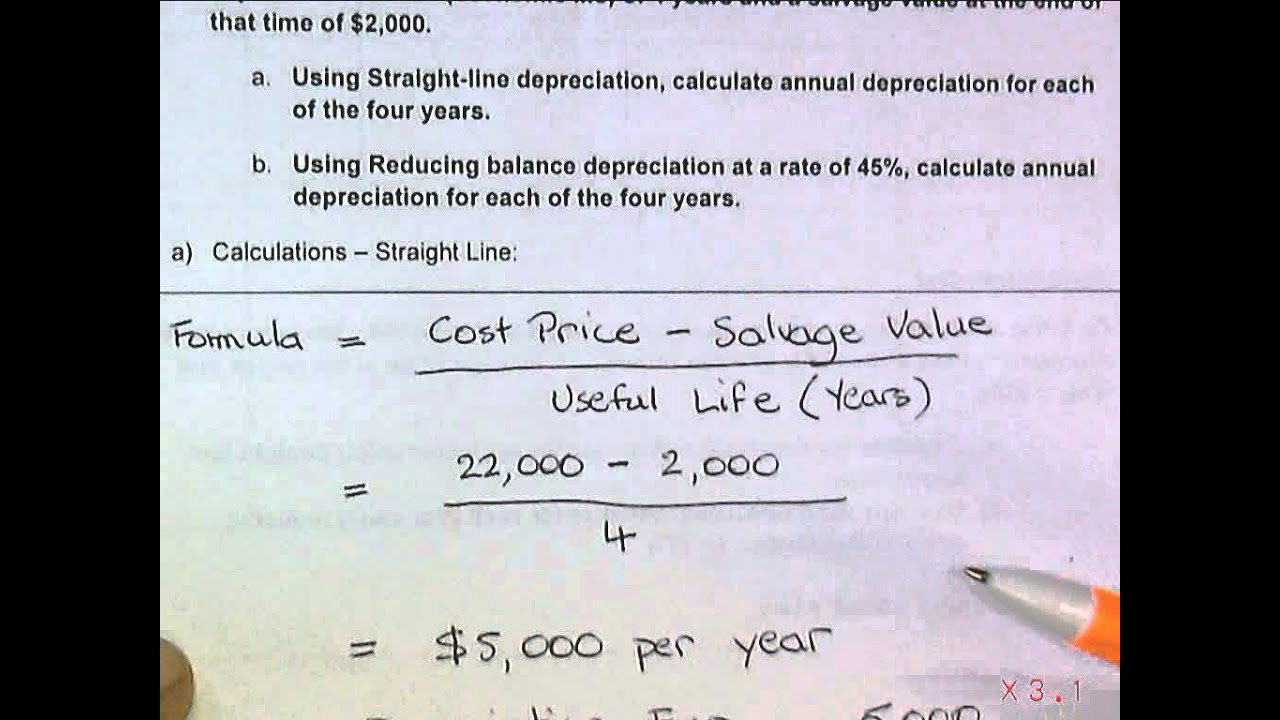

Straight Line Depreciation: Understanding the Straight-Line Depreciation Method for Fixed Asset Depreciation Expense

The 42,000 minus the 40,000 in depreciation, and accumulated depreciation gets us to our residual value of 2,000. To calculate the straight line basis, take the purchase price of an asset and then subtract the salvage value, its estimated value when it is no longer expected to be needed. Then divide the resulting figure by the total number of years the asset is expected to be useful.

Accelerated depreciation vs straight-line depreciation

On the balance sheet, depreciation affects both the assets and the accumulated depreciation accounts. When a company purchases a capital asset, it is recorded at its original cost in the fixed assets section. The accumulated depreciation, which is a contra asset account, is used to represent the total depreciation expense that the asset has accumulated over its useful life. Now let’s look at the good way when we are using depreciation expense.

إقرأ أيضا:Sizzling Hot 100 kostenlose Spins kein Einzahlungscasino Bet365 Deluxe Gratis zum besten geben ohne AnmeldungHow to calculate straight-line depreciation

Additionally, you can calculate the depreciation rate by dividing the depreciation amount by the total depreciable cost (purchase price − estimated salvage value). This means taking defining indemnity in the context of actual cash value calculations the asset’s worth (the salvage value subtracted from the purchase price) and dividing it by its useful life. This number will give you an asset’s annual depreciation expense.

Therefore, Company A would depreciate the machine at the amount of $16,000 annually for 5 years. Company A purchases a machine for $100,000 with an estimated salvage value of $20,000 and a useful life of 5 years. A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation. Our goal is to deliver the most understandable and comprehensive explanations of financial topics using simple writing complemented by helpful graphics and animation videos. At Finance Strategists, we partner with financial experts to ensure the accuracy of our financial content.

- Note how the book value of the machine at the end of year 5 is the same as the salvage value.

- This is especially important for businesses that own a lot of expensive, long-term assets that have long useful lives.

- It is considered more accurate in reflecting an asset’s wear and tear than the straight-line approach, especially for assets whose usage significantly fluctuates.

- Salvage value, the estimated residual value of an asset at the end of its useful life, plays a crucial role in straight-line depreciation calculations.

Understanding Salvage Value in Straight-Line Depreciation Formula

Note how the book value of the machine at the end of year 5 is the same as the salvage value. Over the useful life of an asset, the value of an asset should depreciate to its salvage value. With straight-line depreciation, you must assign a “salvage value” to the asset you are depreciating. The salvage value is how much you expect an asset to be worth after its “useful life”.

إقرأ أيضا:Reactoonz Slot -App Slot Spielbewertung, Kostenloses SpielenSo we would show the net book value just alongside all of our assets there. We’re leaving the truck, the value of the truck that we paid for at its historical cost but then we lower it with this accumulated depreciation over its life. So let’s pause here and on the next page we’re going to continue this example and kind of follow the whole life of this asset, alright? With the double-declining balance method, higher depreciation is posted at the beginning of the useful life of the asset, with lower depreciation expenses coming later.

إقرأ أيضا:Booming online casino roman legion GameThe straight-line method is advised also because it presents calculation most simply. It has a straightforward formula and an approach that reduces the occurrences of errors. All these factors make it a highly recommended method for calculating depreciation. While there are various methods to calculate depreciation, three of them are more commonly used. The depreciation expense is charged in full in all accounting years other than the first and the last accounting year.

This also indicates that there are two years yet remaining to carry out the depreciation of $3,000. All the above calculation is representative of the book value of the equipment as $3,000. However, the company realizes that the equipment will be useful only for 4 years instead of 5. Residual value is the salvage value or the value at the end of the life of the asset.